Kenorland Minerals: Simply The Best Prospect Generator

As Kenorland is the posterboy of a very high profile prospect generator play, with one of the best risk/reward ratios in my view, this is fully understandable. The only adjustment that could weaken the team somewhat is the departure in good standing of co-founder and President Francis MacDonald. He will elaborate about his motives in this article.

It is my personal opinion that a prospect generator like Kenorland needs a Tier I discovery in order to create a Reservoir Minerals-like effect, and for now they are working hard on this. Their Regnault target, a grassroots discovery and located at their flagship Frotet project in Quebec, part of the 20/80 JV with Sumitomo where Kenorland is the operator, keeps gradually expanding on good drill results, causing Sumitomo to fund new exploration budgets. Another interesting development occurring this summer was the optioning out of Tanacross to another major miner, Antofagasta, which wasted no time, budgeted C$2M for exploration and put Kenorland to work last month as the operator.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

Please note: the views, opinions, estimates, forecasts or predictions regarding Kenorland’s resource potential are those of the author alone and do not represent views, opinions, estimates, forecasts or predictions of Kenorland or Kenorland’s management. Kenorland Minerals has not in any way endorsed the views, opinions, estimates, forecasts or predictions provided by the author.

Kenorland Minerals is one of the more puzzling juniors I’m covering. As I mentioned many times, this company probably is the best prospect generator out there, with very smart management which developed their own novel exploration strategy designed to find Tier I assets. It is backed by premium funds and never has any shortage of cash, has option agreements and JVs with the best and largest producers in the mining industry, and has extensive land packages of the highest quality in the best jurisdications available. Their flagship Regnault project is advancing in the desired direction, showing extensive mineralization, persuading Sumitomo to keep funding new exploration programs in the blink of an eye. Despite all this, the share price has a hard time ascending above the C$0.70 IPO price, and it is my strong conviction that it keeps trading around this price due to strong shareholder support, as many other stocks keep losing ground since the summer.

As prospect generators in my view need a Tier I discovery as mentioned, the wait is on for Regnault to grow into one, or other projects that generate one. Kenorland is built and wired for discovering Tier I projects, so if any junior can do it, it is this company in my opinion. As the task at hand isn’t easy, I understand the need to be patient as an investor. Sometimes when thinking out of the box, and keep in mind I’m not a big admirer of flavour of the day management, I do wonder if they shouldn’t finally look into other Quebec-based hot metals like lithium, as they know this jurisdiction very well, Quebec is covered with pegmatites, and recently a very impressive discovery has been made in this regard (Corvette project, owned by Patriot Battery Metals (PMET.V)).

After all these contemplations, it is time to discuss the ongoing affairs. On October 21, 2022, the company announced the resignation of co-founder and President Francis MacDonald. According to the news release, he decided to pursue other opportunities, although he will continue to support through a lead technical advisory role. CEO Flood, who will also be President, had this to say about the different path taken by his good friend, with whom he started the Kenorland adventure:

“Francis, myself, and two other co-founders, Scott Smits, Vice President of Exploration, and Dave Stevenson, Chief Geoscientist, created Kenorland in 2016 with the vision to become one of the leading exploration companies in the business. Together, along with the rest of the Kenorland team and with strong support from our shareholders, we’ve accomplished that goal, and while there is still immense value for us to create through continued exploration and discovery, we support Francis’ decision to pursue other opportunities. On behalf of Kenorland, we thank Francis for his significant contributions and wish him all the best on this next chapter of his career. At the same time, we look forward to his continued involvement in the Company as a lead technical advisor.”

It was good to see there was full respect and understanding for each other. Nevertheless, I’m not typically overjoyed when I see a founder leaving a company before it is a resounding success, and wanted to know more so I contacted Francis for more color on his departure. He couldn’t elaborate as much as he wanted as disclosure rules regarding future employers prevented this, but he was willing to share this with the audience: “It was not an easy decision to leave Kenorland after putting so much time and energy into the company for the last 6 years. I’ve enjoyed every minute of working closely with Zach Flood, Scott Smits, Dave Stevenson, Janek Wozniewski, Alex Gallardo, Vytas Banys, Enoch Kong, Andy Orr, and Mikhail Minin to build this company into one of the premier project generating companies in the mining business. The decision to leave was multi-faceted, but the main reason is that my work-life balance was not where I wanted it to be. We set the company up to have a very flat management structure which required constant attention to many different things.

I’ve been living in Europe for the last three years which has required me to overlap with Vancouver time. I tried to limit my overlap between 5pm and 8pm European time, but inevitably this overlap spilled into my evenings and late nights. My wife and I had a baby 1.5 years ago and it was getting to the point where I would hardly see either of them because of my working hours. Looking ahead into the future, it was hard to see this being a sustainable lifestyle so I decided it was time for a change. I had another opportunity presented to me, which probably facilitated the decision to leave Kenorland, but I think this would have been the eventual outcome based on my home life. The new opportunity may not give me the work-life balance I’m looking for in the short term, but it’s also a clean slate – I can organize things differently and hope it works for me a bit better. I look forward to being involved in Kenorland as a technical advisor and a supportive shareholder.”

This is all very understandable, and fortunately had nothing to do with Kenorland proceedings. Regarding Kenorland business, on October 24, 2022, Kenorland announced the formation of a 49-51% JV with Sumitomo at the Chicobi project in Quebec, which completed their earn-in obligations. Sumitomo spent C$4.9M in exploration expenditures, and now the JV will fund further exploration on a pro-rata basis, with Kenorland continuing as the operator. For now, a C$1.5M program is funded completely by Sumitomo, and involves sonic drill holes for geochem sampling. Kenorland has completed quite a bit of work since 2019, as to date, 1,908m of diamond drilling, and three phases of sonic drilling, totaling 441 drill holes have been completed across the project producing 1,500 samples for gold grain counts, heavy mineral concentrate assays, and till geochemistry assays.

Although there were no significant intervals from the diamond drill holes reported by Kenorland, Sumitomo obviously saw enough data of interest to form the JV.

This was not the only deal they did this summer, after closing an option agreement in July with Antofagasta regarding Tanacross they disclosed the selling of their shelved Wheatcroft Project in Manitoba to Jayden Resources on October 3, 2022. Kenorland received 5.55M shares of Jayden (trading at C$0.17 at the time), a 3% NSR and C$125k in cash at closing. In the event of Jayden issuing more shares in capital raises, Kenorland receives additional shares to get them at least at 9.9% ownership of Jayden’s outstanding common shares. Wheatcroft is the same glacial till style project as most of the other projects in Kenorland’s portfolio, and Kenorland will be the operator of a property wide till geochemical survey during the fall of this year. A large 200x800m arsenic and gold geochemical anomaly has been defined, and this will be further explored with this survey.

I consider this a nice and unexpected windfall, as CEO Flood never bothered to discuss Wheatcroft with me, as it was inactive and not scheduled to do work on soon.

This sale wasn’t the only recent financing activity for Kenorland. After announcing a C$6.3M non-brokered private placement at September 9, 2022, they closed it at C$7.49M on September 19, 2022, using the overallotment option almost in full (proceedings would have been C$7.7M). As a result, 10.7M shares were issued at a price of C$0.70, with no warrants which shows real strength in these uncertain conditions. JV partner Sumitomo acquired 1.08M shares in this round, maintaining their 10.1% interest in the company. As always, there is a 4 month and 1 day holding period, so keep this date marked in your agenda as a habit. Although Kenorland raised at low levels (even equal to the last pre-IPO round), creating substantial dilution for existing shareholders, the golden rule for juniors is always “when cash is offered, take it”, as it can be unavailable when times get worse, or even worse when you really need it. Since the share price didn’t do much better all year, CEO Zach Flood didn’t have many options to raise at higher prices in my view.

In this case it is a slight disadvantage for Kenorland to have their flagship projects all under earn-in agreements/JV’s, so they don’t fund them themselves but their partners. Otherwise the company could have raised under flow-through regulations for Quebec projects, applying a 35-40% FT premium. Besides Sumitomo, all other major holders participated as well in the financing, expressing their support, and Haywood came up with about C$1.2M as well, collecting C$76.5k in finders fees. This is not a big surprise as John Tognetti, the founder and Chairman of Haywood, is a large shareholder, and financed Kenorland since inception.

The financing wasn’t the only thing Kenorland Minerals completed this summer, as it also struck a deal with Antofagasta regarding the Tanacross copper-gold project in Alaska, and announced a new R6 vein discovery in July, releasing the results of a small batch of assays for 5 drill holes. The Tanacross deal was something that was in the works since May 2022, and was a bit of a surprise as management never discussed this, and was still waiting for results from surface exploration including geochemical and geophysical surveys that were completed in June.

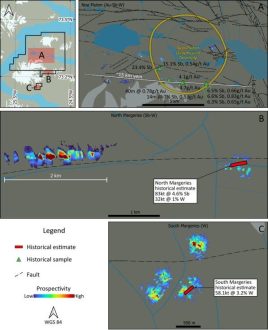

As for the specifics, Antofagasta was granted the option to earn-in a 70% interest by paying Kenorland US$5M in total, and spending US$30M on exploration expenditures over 8 years, plus completing a NI43-101 compliant Preliminary Economic Assessment (PEA). Kenorland will be the initial operator during the period leading up to the 70% interest, and Antofagasta is required to spend at least US$1M in year one. Once Antofagasta has earned its 70% interest, Kenorland and Antofagasta will form a 30/70 joint venture. If either party’s interest in the joint venture falls below 10%, that party’s interest will be converted to a 2% NSR, one quarter of which can be purchased by the other party for US$2M. To get an idea of the scale of Tanacross (45,900ha), see the maps below, taken from the NI43-101 project report:

This is another rare and monumental earn-in agreement, which would send any nano cap much higher, but unfortunately it is business as usual for Kenorland, and investors do not even raise an eyebrow anymore. Let’s hope Tanacross could provide the company with a Tier I discovery, as it certainly has the scale and the potential for it. After asking about the pending results of Tanacross, CEO Flood answered the following: “We will be reporting on results from our surface programs towards the end of 2022 or early 2023.”

Let’s have a look at the July drill results of flagship project Regnault now, published at July 11, 2022.

This batch completed the results of the 2022 winter program, and involved the assays of the remaining 5 of 25 drill holes completed, containing the last 2,840m of 10,880m completed in total. The highlights looked like this, involving several new vein discoveries:

- 22RDD133: 6.65m @ 19.50 g/t Au incl. 1.06m @ 98.34 g/t Au at R6 (new vein discovery)

- 22RDD135: 1.70m @ 25.00 g/t Au incl. 0.45m @ 87.00 g/t Au at R1

- 22RDD135: 5.00m @ 5.46 g/t Au incl. 0.90m @ 21.39 g/t Au at R8 (new vein discovery)

CEO Zach Flood was pleased with these results: “Results from these new vein discoveries are easily comparable to some of the best results from the R1 structure, which we’ve been drilling off since the initial discovery in 2020. This is great news for the Joint Venture and we look forward to further results from the recently completed summer drill campaign, which was largely focussed on following up these discoveries.”

These newly discovered veins run parallel to the main R1 structure, and Kenorland labeled them R5, R6, R7 and R8, which are represented below in this cross section:

It was good to see hole 133 delivering good intercepts, like 6.65m @ 19.5g/t Au, more than confirming the results of hole 121 which discovered the R6 vein. In general, the discovery of these veins indicates the potential for further sub-parallel structures at depth. When looking at this section, it appears that R5 to R8 could potentially remain open along strike and depth.

He wasn’t the only one excited about these results, as Scott Smits, VP of Exploration showed his enthusiasm as well: “Its hard not to be excited about the steady high-grade intercepts we have received from the first quarter of 2022. Our strategy has been to aggressively step-out along the known trends and explore for additional mineralized structures, constantly growing the mineralized footprint at Regnault. These recent results continue to demonstrate the potential for further growth of this exceptional gold system.”

This was understandable, as this 2022 winter drill program was designed to expand the strike extent along the R2 and R4 trends, testing the down dip extents of the R1 mineralized structure, and explore for additional mineralized structures immediately to the south of R1, so all these additional high grade veins were a welcome surprise. Notwithstanding this, the R1 mineralization was extended during the program by another 100m to the east for a strike length of 950m, and to depths up to 400m, remaining open along strike and depth.

Regarding my back of the envelope estimate for the hypothetical Regnault resource not much has changed, except for the R5-R8 veins which were expanded. The map shows a significant projection of the R5 vein, up to 700m long. As a reminder, the R1 zone is in fact a set of layered veins, but for guesstimating purposes this will be calculated as one zone. This results in an updated, very global back-of-the-envelope estimate on the R1 structure, with an average grade*thickness (or GT as Kenorland calls it) of 5*5 = 25, and arrive for R1 at 950 x 300 x 5 x 2.75 = 3.92Mt, at an average guesstimated grade of 5g/t Au this would mean a hypothetical 630koz Au.

The R2 back-of-the-envelope guesstimate stands unchanged at 700 x 200 x 2 x 2.75 = 770kt, at an average guesstimated grade of 9g/t Au this remains a hypothetical 223koz Au. For the R3 structure it is too early to do any guesstimates, as there haven’t been enough results reported for this particular structure. The R4 structure to the north seems to be consisting of fairly narrow veins as well, 200m long and 225m deep, however not continuous from surface but separate vein structures, so the combined mineralized envelope is guesstimated at 200 x 100 x 2 x 2.75 = 110kt, at an average guesstimated grade of 15g/t Au this could imply a hypothetical 53koz Au.

For the R5-R8 vein set I prefer to simplify things, calculating a single envelope, arriving at a guesstimated tonnage of 700 x 300 x 5 x 2.75 = 4Mt, at an average guesstimated grade of 5g/t Au potentially resulting in 460koz Au. The potential is there to see R6, R7 and R8 developing in full-blown structures of their own, so it is understandable to see Sumitomo sinking more and more cash into the Regnault target. My overall estimate would come in at an hypothetical 1.37Moz Au for now. As this number is conservative in my view, I see clear potential to go to 2Moz in 2023. Such numbers should be able to move the needle for investors, especially in a turning market with improved sentiment, but this is no certainty of course as it still doesn’t have the hallmarks of a Tier I deposit (over 5Moz Au).

However, it definitely isn’t obvious what the goals of Sumitomo are for Regnault, especially when the high grade structures will take lots of drilling to delineate significantly more ounces at depth. This deep drilling might be easier and cheaper to conduct during production, so Sumitomo might seek to fast-track to production once a certain resource threshold is met, probably diluting or buying out Kenorland in a fancy deal, as I don’t see Kenorland funding capex pro rata, being explorers pur sang. But this is all speculation on my behalf of course, let’s wait and see.

Upon completion of the Q1 2022 winter drill program and prior to the announcement of the company’s summer 2022 drill campaign a total of 45,086m had been drilled at Regnault including the initial discovery drill program in early 2020. Drilling is currently underway from the recently announced fiscal 2022 exploration budget, which will include up to 40,000 meters of drilling carried out over two phases: a summer campaign from April to July of 2022, and a winter campaign from January to April of 2023. The company has recently completed the summer drill campaign at Regnault, consisting of 11,903m, and drill results are expected around early November in one batch. This program focused on further step-outs along strike and searching for additional sub-parallel structures to the south. I wondered if CEO Flood was also interested in drilling out R5-R8 more along strike and at depth as discussed. He answered, “This will be the main focus of the 2023 winter drill program when we can utilize the ice to drill on the lake. This anticipated program will include around 25,000m of drilling.”

Kenorland has also commenced a 2,500m drill program at their Cressida target, more to the northwest area of the Frotet project. This target can be observed below, along strike of the nearby (2.5km) Troilus deposit:

The sampling results clearly highlight the Cressida target, so this seems logical. As a reminder, the entire Frotet project is part of the Sumitomo JV where Kenorland is the operator. Drilling at Cressida is expected to be completed by mid-July, and the results are expected around early November with the rest of the summer results. I discussed the property areas with CEO Flood a while ago, where he mentioned that the zones not currently controlled by Kenorland/Sumitomo in between Regnault and Cressida were previously owned but dropped as sampling sterilized it.

Regarding other projects in Kenorland’s portfolio, the second most important project is Healy (Alaska). After a first drill program returned not very impressive results, management still has no immediate plans to explore Healy at the moment, however they continue to look at alternative paths forward which could still advance the project.

Kenorland also completed a VTEM survey at the Hunter project in Quebec (optioned to Centerra Gold), and a LiDAR survey and mapping at South Uchi (optioned to Barrick). The current status on these projects is as follows: at Hunter a property-wide sonic drill-for-till program will be carried out next month. At South Uchi, Barrick will be following up on the 2021 property wide till geochemical survey with further exploration. Multiple discrete gold anomalies were identified and have been prioritized for follow-up exploration in 2022. For 2022, Barrick has approved a C$1.8M budget to complete infill glacial till geochemical sampling, within the regional As-Sb+/-Au anomaly, on a 350m by 150m spaced grid. The follow-up survey is planned to be carried out between mid-June and mid-August. CEO Flood told me Barrick was very active on South Uchi this summer and they expect to receive more information into the fall.

Since till sampling, boulder prospecting, airborn magnetics and an IP survey have been completed at Deux Orignaux (Chebistuan), further targeting is on its way. According to CEO Flood, they proposed a program, but are still waiting for an answer from Newmont on this proposed program.

The treasury currently stands at about C$10M, and management is contemplating budgets for 2023 on exploration advancing their own projects including funding its joint venture commitment at Frotet, further exploration in Alaska, and additional generative exploration.

Conclusion

Although the share price of Kenorland Minerals doesn’t really represent the increasing value of the Regnault target and the recent deals, it holds up pretty well where most competitors keep declining. Kenorland formed a JV with Sumitomo at Chicobi, sold Wheatcroft for C$1.1M, and closed a C$7.49M non-brokered private placement, supported by their impressive set of backers, signed an interesting earn-in agreement with Antofagasta over Tanacross, adding another major to their stable of partners, and released the last, strong drill results of the winter drill program for Regnault. The departure of President Francis MacDonald will be felt as he played a major role in the formation, asset selection, exploration strategy and research of Kenorland, but it is good to see he keeps involved as a lead advisor.

The latest summer drill program is completed, with results coming up early November, and I expect further expansion of mineralization which I estimated already at a hypothetical 1.37Moz Au. In my view, Kenorland was, is and will be the ultimate example of a prospect generator, hunting for Tier I assets, and it seems only a matter of time before they will hit something really big, which will be the important catalyst in my view here. How much time is needed will be the million dollar question but Kenorland isn’t hired by Barrick, Newmont, Antofagasta, Sumitomo, Centerra and Freeport McMoRan for significant option agreements and JVs for no reason.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter, in order to get an email notice of my new articles soon after they are published.

Disclaimer:

The author is not a registered investment advisor, and currently has a long position in this stock. Kenorland Minerals is a sponsoring company. All facts are to be checked by the reader. For more information go to www.kenorlandminerals.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Swiss Resource Capital AG

Poststrasse 1

CH9100 Herisau

Telefon: +41 (71) 354-8501

Telefax: +41 (71) 560-4271

http://www.resource-capital.ch

CEO

Telefon: +41 (71) 3548501

E-Mail: js@resource-capital.ch

![]()